Opinions on the state of the current real estate market largely vary along the dichotomy of optimists and pessimists. For the glass-half-full types, the recent uptick in pending sales and drop in interest rates is a clear sign that the worst is in the past. For the glass-half-empty types, they are saying "not so fast!"

As is true of most opposing perspectives, the truth often lies somewhere in the middle.

Just to be transparent, most of the data is still pointing to a very weak real estate outlook. Sales are still down from historic highs, and rates are still higher than they have been in decades. Is this really "old news"? Maybe, maybe not.

The energy right now is on the "new news". It brings a lot of hope for the soft landing that seemed so out of reach a few short months ago. The reality is a little more complex.

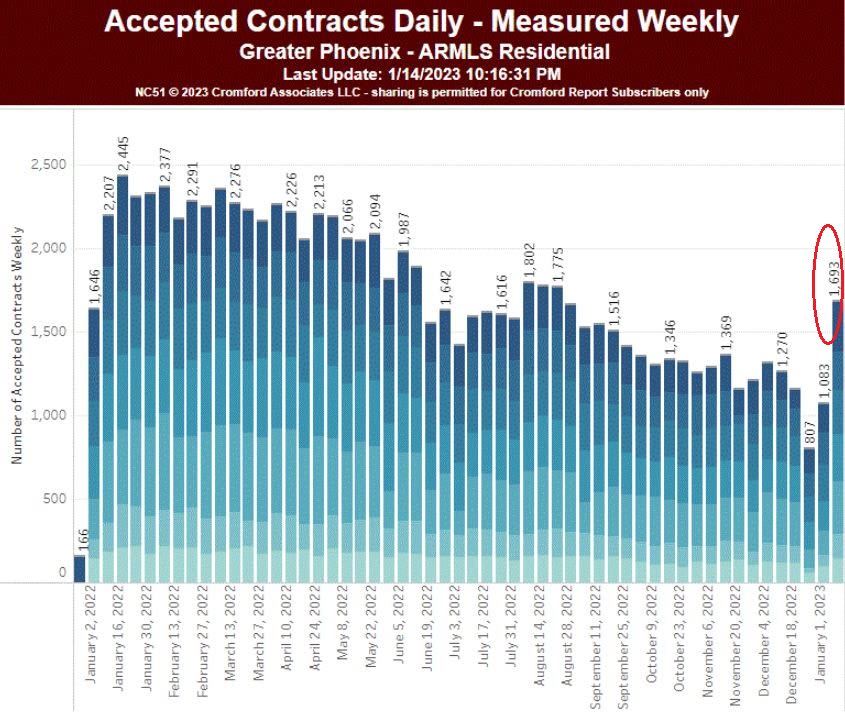

The Cromford Report is a local team of analysts that compile essential real estate data for the entire Phoenix area. There has been some interesting data in recent weeks. It's way too soon to suggest that any of this data says a turnaround is imminent. But it is curious to look at. For instance, coinciding with the easing of interest rates, we have seen a corresponding bump in accepted contracts. The chart below from Cromford demonstrates the bump.

What we can interpret from Accepted Contracts Daily chart at this time is that there were a number of buyers on the sidelines ready to jump as soon as they saw an opportunity to lock in a lower mortgage rate. While indicative of continued pent-up demand, this won't become a "trend" until we see the pattern repeat over several cycles. We'll need to be patient to see if this becomes a long-term turnaround in the market.

“This recent low point in home sales activity is likely over,” said NAR Chief Economist Lawrence Yun. “Mortgage rates are the dominant factor driving home sales, and recent declines in rates are clearly helping to stabilize the market.” Of course, Mr. Yun is speaking of the national trends. Here in the Valley, we are seeing a mixed bag.

Take for instance the Cromford Market Index. If you are not familiar with this index, it measures the balance between buyers and sellers. A CMI of 100 would be an exactly balanced Market. Higher than 110, and it becomes a Seller's Market. Below 90, and it becomes a Buyer's Market.

If you notice from the chart above, we still have 10 communities with a CMI over 110, with three communities in the "balanced" territory between 90-110 (Gilbert, Peoria, and Surprise). The rest are in buyers' markets, but on an upward swing (look at Queen Creek up 24%!). According to the Cromford commentary, what's propping up the luxury areas is the fact that sellers are retreating, meaning there is less inventory to meet the demand from buyers. This puts upward pressure on prices that defy the conventional wisdom that would normally apply in the current interest rate environment.

According to Cromford analysts, "the market is more favorable to sellers than we expected in December and downward pressure on pricing has been largely eliminated, except in a few market segments."

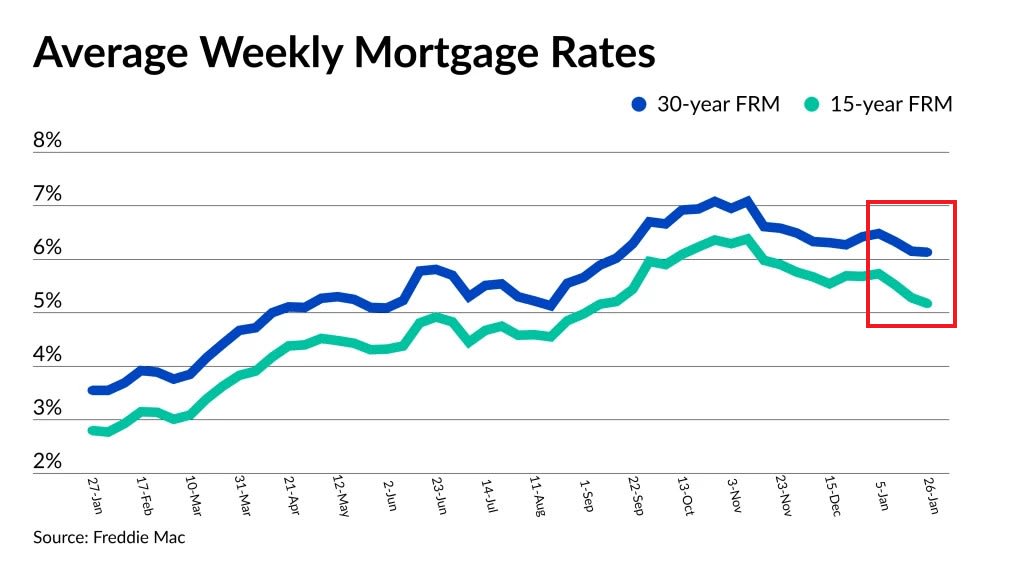

For the mid-range markets, mortgage rates are a huge culprit in the weakening of the real estate market. Buyers who were already financially stressed to afford a home in a market with wildly increasing home prices simply had no way to combat the added pressure that borrowing costs added to the equation. Rates have definitely improved SOME compared to the last few months. However, in the context of the extremely low rates we have enjoyed over the last decade, rates are still scarily high. What is easing some fears, however, is not the decrease in the rates, but the relative stability we have seen over the last weeks. Wild swings scare buyers, plain and simple.

Interestingly enough, this combination of lower and more stable rates PERFECTLY coincides with a noticeable shift in purchase mortgage applications. This week saw purchase apps tick up to the highest levels since August. Putting this together with the increased pending transactions we discussed earlier, it's easy to see why the optimists are feeling pretty confident.

As a Realtor with decades of experience, one of the benefits of having been through up and down markets is the historical perspective. I've learned that drawing sweeping conclusions based on a short run of data usually leads to disappointment. Rates could go back up, even higher than before (although we hope not!). Or they could stay in a tight range for a while, waiting for more economic support. But until we see sustained shifts in the market, it's better to keep one foot on either side of the line between pessimism and optimism.

Just consider this. Housing costs are part of the inflationary pressures and even had an outsized impact on inflation measures, especially in Phoenix and other sunbelt markets that saw extraordinary increases in home values. If they too much "irrational exuberance" driving a housing recovery, it could trigger more painful rate increases.

Below are some key statistics for several communities in the Greater Phoenix area.

Ultimately, real estate is just one factor in a host of other factors that are driving the Fed decisions on interest rates; even for those cash buyers who aren't concerned with mortgage rates, consumer sentiment and optimism about the economy and real estate investment may have some bearing on decisions to buy a home in 2023. That said, the data shows us that buyers are still bullish on the sunbelt and Phoenix in particular. We just need to see how interest rates play out and if sellers will come out to play this spring.

_____________

We are here to help! If you want to find out how much your home is worth in this strong market, email me at [email protected]. We would be happy to help you determine if the time is right for you to sell your home or buy a new home.